In this video, you get answers to these questions:

- What is a phantom stock plan?

- Why would people want to use a phantom stock plan?

- What are some problems with using a phantom stock plan?

Introduction

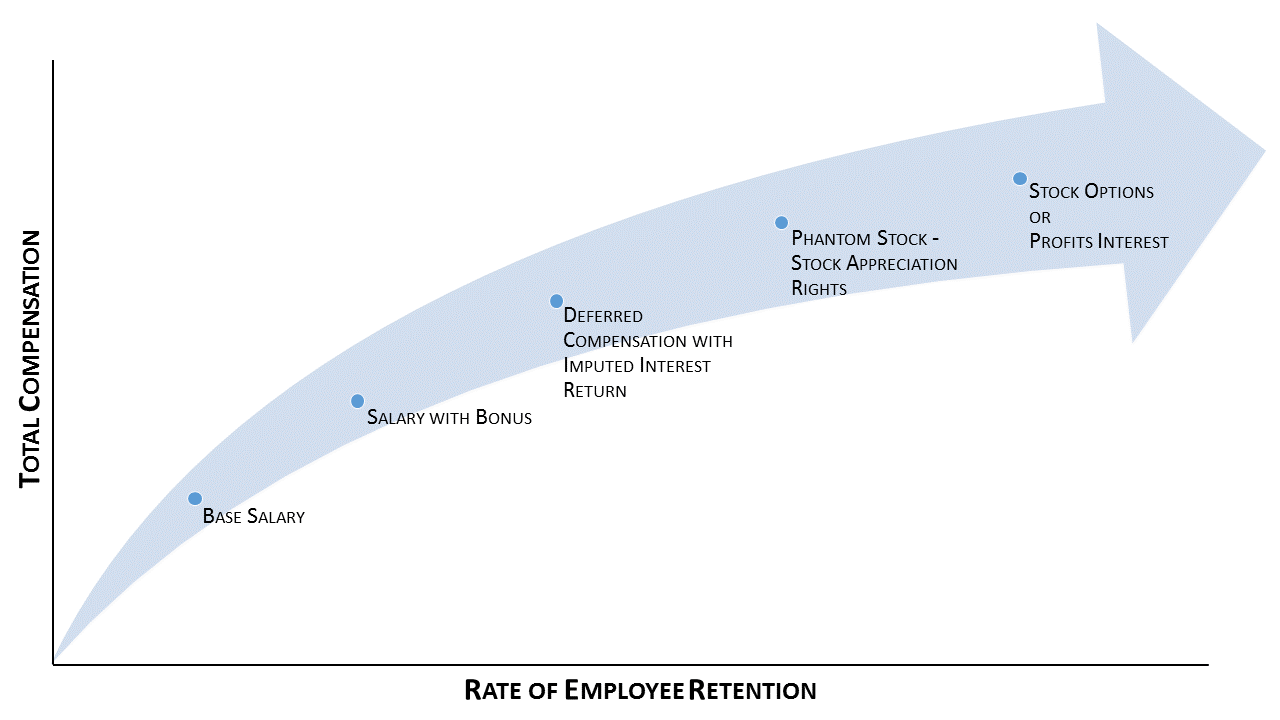

In a dynamic economy with rapidly developing technological advancements, companies often struggle to keep their key employees from moving to new opportunities. Retention of these employees must involve some type of equity participation. Base salary, and even a salary with bonus opportunities, just doesn’t cut it in hyper-competitive business sectors. Companies must be willing to share profits with key employees to retain them over the long-haul and to minimize attrition costs.

Solution

One of the following compensation tools can make all the difference to the future success of your company when human capital is at a premium, assuming you are willing to share ownership with key members of management, sales or production:

Deferred Compensation with Imputed Interest Return

A level of income above base salary is set aside by the company, earns interest during the deferral period and is payable to the employee at a given point in the future. Non-qualifying plans permit companies to offer deferred compensation only to their most valuable employees rather than being required to offer the same plan to all employees as required under ERISA (here, 401k plans are the most obvious example). In the case of non-public entities, the tax deferral of such compensation only works if the company can demonstrate a high likelihood that a top producer or key manager might leave for a competitor (the “substantial risk of forfeiture” rule of the IRS).

Phantom Stock – Stock Appreciation Rights

In one sentence, this is a right to a percentage of the appreciation in the value of the company over a baseline value established at the time of commencement of the employee’s right. Upon sale of the company, the employee’s compensation is based upon the value of the company’s stock or the appreciation in value of the stock since the phantom stock award was made.

Stock appreciation rights (SARs) and phantom stock are very similar concepts. Both concepts are bonus plans that grant not stock but rather the right to receive an award based on the value of the company’s stock; hence, the terms “appreciation rights” and “phantom.” SARs typically provide the employee with a cash or stock payment based on the increase in the value of a stated number of shares over a specific period of time. Phantom stock provides cash or stock bonuses based on the value of a stated number of shares, to be paid out at the end of a specified period of time, and are free from the participation, funding, vesting and fiduciary responsibilities imposed upon qualifying plans under ERISA. Typically, receipt of phantom stock is non-taxable to the employee until the cash is paid out, generating ordinary income for the employee but a deduction for the company. Phantom stock initiatives are usually less expensive to implement than formal stock option plans.

Stock Options

These options take two different forms: non-qualified stock options and incentive stock options. Options are normally granted for a strike price equal to the fair market value of the underlying stock to avoid tax at the time of grant. A company grants an employee options to buy a stated number of shares at a defined price, referred to as the “grant” or “exercise” price. Typically, these stock options vest over a period of time or once certain individual, group, or corporate goals are attained. Some companies set time-based vesting schedules but allow options to vest sooner if performance goals are met or the sale of the company occurs (generally known as “cliff vesting”). Once vested, the employee can exercise the option at the grant price at any time over the option term up to the expiration date.

Options granted under an employee stock purchase plan or an incentive stock option (ISO) plan are statutory stock options. Stock options that are granted neither under an employee stock purchase plan nor an ISO plan are nonstatutory stock options. When an employee exercises an ISO, the spread on the exercise price and the market value of the stock is taxable to the employee as ordinary income, even if the shares are not yet sold, and generating a deduction for the company. An ISO enables an employee to (1) defer taxation on the option from the date of exercise until the date of sale of the underlying shares, and (2) pay taxes on his or her entire gain at capital gains rates, rather than ordinary income tax rates. Employees who are granted stock options hope to profit by exercising their options to buy shares at the exercise price when the shares are trading at a higher price.

Restricted Stock

Actual outright stock ownership is transferred but is restricted for a defined period of time by providing for a nominal buy-back price in the case of termination of employment prior to the lapse of the restriction. Restricted stock plans provide employees with the right to purchase shares at fair market value or at a discount, or employees may receive shares at no cost from the company as a mean of retention. The shares employees acquire are subject to vesting restrictions, such as length of service, with three to five years being typical. Time-based restrictions may lapse all at once or gradually, or the company could, for instance, restrict the shares until certain corporate, departmental, or individual performance goals are achieved regardless of the employee’s length of service.

With restricted stock units (RSUs), employees do not actually receive shares until the restrictions lapse. In effect, RSUs are like phantom stock settled in shares instead of cash. RSUs are considered compensation, so the employee will pay ordinary income tax rates on their value at the time of vesting (unless the employee makes the Section 83(b) election and pays income tax within 30 days of receiving the stock grant, allowing the employee to pay capital gains tax rates on any stock appreciation from the time of grant to the time of sale).

Conclusion

One of these employee retention techniques can prove valuable in the company’s effort to retain top talent. Stock-based compensation can provide employees at all levels the incentive to remain with the company because, if for no other human motivation, they will share in its growth. If done properly, stock-based compensation can work to align employees’ interests with those of the company’s founders, leaders, shareholders and investors while allowing the company to minimize cash outlays and the burn rate. Equity participation for employees is governed by a multitude of rules and regulations, so caution is encouraged for any company looking at implementing any of these plans. Be sure to connect with your legal and accounting advisors on key considerations, including securities and employment law compliance (such as exemptions from registration and notice requirements, as wells as issues involving dilution, excessive compensation or option re-pricing, etc.), federal tax consequences (such as tax treatment, tax reporting and issues of deductibility, etc.), accounting practices (such as expense charges, deductibility of value of options or imputed interest of deferred comp, dilution, etc.), and corporate law compliance and considerations (such as corporate authorization, conflicts of interest and whether fiduciary duties are triggered, etc.).

Video Transcript

I’m Aaron Hall, an attorney in Minnesota. You can learn more about me at aaronhall.com.

Today I’m talking about phantom stock plans. What is a phantom stock plan? It’s essentially a contract where the owner of it, or the beneficiary of it, can get a buyout of the stock plan at a later date, depending on the value of the company at that time. Typically, the company is valued through a independent professional appraisal service, so there is some cost associated with that.

Why would people want to use a phantom stock plan? Well, it’s typically a way for a business owner to give some ownership interest to an employee without actually transferring real ownership.

Now, sometimes that works. The employees say, “Hey, this is great. I wasn’t going to get anything but my wages. Now I’m going to get actual value of the company upon the sale of these interests.” Well maybe it’s… And you might say, “Well, what kind of sale?” Maybe it’s an acquisition of the company, maybe it’s closure of the company. Maybe there are other timetables built in there. Either way, it allows employees to get some value as though they own the company, and so the more the company appreciates in value, the more the employee benefits.

Well, what are some problems with it? For one, since this is a form of delayed compensation, it’s governed by ERISA. That’s E-R-I-S-A, a federal statute that governs wages and retirement and delayed compensation. So, you have to make sure that your phantom stock plan is compliant with ERISA. The other problem is sometimes employees were just as motivated by wages. They didn’t actually need this, and so it’s now an additional complication. Finally, some employees say, “This isn’t actual ownership. Hey, it’s nice, but it really doesn’t motivate me like actual ownership would do.”

Many times when small business owners are thinking about setting up a phantom stock plan, I talk with them about what do you actually want to accomplish, what are your goals. And we figure out, is there a way to do this without ERISA regulatory issues. Either way, your best advice is talk with an attorney and focus on your business goals first, and that will help the attorney determine whether a phantom stock plan or some other arrangement is the best way to accomplish your goals.

To learn more, click the description below. There are a number of links and additional information on my website.